CONTENT MARKETING

FOR FINANCIAL PROS

CONTENT MARKETING

FOR FINANCIAL PROS

It is all a mystery.

{kind=link}

As if we don’t have enough investing decisions to deal with, we now are facing another one with the introduction of the TFSA (Tax Free Savings Account). The most common question in February? “Which is better TFSA or RRSP�

As if we don’t have enough investing decisions to deal with, we now are facing another one with the introduction of the TFSA (Tax Free Savings Account). The most common question in February? “Which is better TFSA or RRSP�

Here’s the good news - it doesn’t have to be an either or choice.  Why not do both? If both, in what proportion should you divide your contributions? In order to make an informed decision, let’s quickly review the main features of each program.

Â

Tax Free Savings Account (TFSA)

Maximum contribution is $5,500 per year (up from $5.000 for 2009-2012) and must be made by December 31st of the year of contribution.

There is carry forward room for each year in which the maximum contribution was not made.

The deposit is not tax deductible, but the funds accumulate with no income tax payable on growth.

Withdrawals may be made at any time on an income tax free basis. Withdrawals create additional deposit room commencing in the year after withdrawal.

Registered Retirement Savings Plan (RRSP)

Â

Â

Contribution is tax deductible from earned income, and the funds accumulate on a tax deferred basis.

All withdrawals are taxable as income at top rate of tax based on earnings in the year of withdrawal.

RRSP ends in year contributor turns age 71, when the RRSP must be converted to a Registered Retirement Savings Plan or life annuity and taxable income taken.

Now that we have reviewed the provisions of each program, let’s try and analyze what program works best for us and in what proportion.

Both programs provide for no tax on the earnings on the contributions, no difference there. However, only the TFSA allows for withdrawals with no tax - ever. If you are not reinvesting the tax savings generated from your RRSP contribution, the only thing you gain is an increase in consumer spending created by the tax saved. The truth is, however, that the tax deferred is really a loan from the government. Although, they don’t charge interest on this loan, the loan must be repaid at some point in the form of taxes on withdrawal.  And like most things in life, that point usually comes when you can least afford it, like when you quit working, or require funds for an emergency.

Be careful not to over value your RRSP balance. It is important to remember that the balance will be reduced by the tax payable. If you are certain that you will retire in a lower marginal tax bracket than you are now, then the RRSP makes some sense.

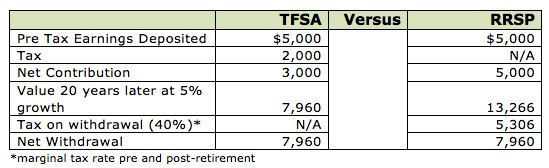

This is also true if you routinely reinvest the tax savings but otherwise, at the end of the day, there is no difference in the final results of the two programs. This can be illustrated in the table below:

Both programs lend themselves very well to each other. If you refer to the features of each listed above, the RRSP’s have to be converted into income starting no later than the contributors age 71. Assuming retirement at age 65 (yes, some people still do that), there are 6 years that bridge income will have to be provided, and what a better way than to have that income paid from a source that is completely free of tax (TFSA)? At the same time, the requirement to pay tax on withdrawing from an RRSP helps to ensure that those funds will actually be saved for retirement. RRSP’s were never designed to be a “rainy day fundâ€, but that purpose is well served by a TFSA.

If you can contribute the maximum to both – GREAT! If not, you should still take advantage of both programs. Try to establish a ratio of contribution that you are comfortable with and go with that. Remember, you can always change the ratio from one year to the next, and whatever plan you don’t maximize this year, your contribution room going forward will allow you to catch up later.

While the rules governing TFSA’s are relatively simple, this is not true with RRSP’s and is beyond the scope of this article. It is best to fully discuss the benefits and restrictions of each of these options before investing.

Please call me if you think you would like to discuss your personal needs or please feel free to use the social sharing buttons below to share this article with a friend or family member you think might find this information of value.